Understanding Seller Concessions in Northern Virginia's 2026 Market

A buyer's agent calls you two days before closing and asks if you'll cover $12,000 in closing costs. Do you say yes because you're scared the deal will fall apart, or do you know enough about seller concessions to negotiate from a place of strength instead of panic?

That phone call is happening more often in Northern Virginia right now than it did three or four years ago, and I want you to understand exactly what's going on before it happens to you.

Seller concessions are simply money or credits you agree to give the buyer at closing, usually to cover their closing costs, sometimes to buy down their interest rate, occasionally to handle a repair instead of doing the work yourself. They are not a sign that something is wrong with your house. They are a negotiating tool, and in this market, a common one.

Here's what's actually happening on the ground. Builders across the region are offering aggressive rate buydowns and closing cost credits right now, which means resale sellers are increasingly having to offer similar concessions or make sure their home's roof, HVAC, and appliances are updated enough to compete with the peace of mind a new build offers. I'm seeing this play out firsthand with clients in Ashburn and Chantilly, where new construction sits right next to resale inventory, and buyers are doing the math to determine which option actually costs less over the life of their loan.

It also depends heavily on what you're selling and where. In Reston, for example, detached homes are still moving with real strength, and buyers are competing for them, while attached homes and condos are sitting in a more patient market where concession conversations come up far more often. I tell my sellers this all the time: don't assume your situation matches your neighbor's. A single-family home in Vienna near the Silver Line is playing a completely different game than a townhome in Sterling.

Loudoun County has its own flavor of this conversation too. It remains the nation's data center capital, and the influx of high-paying tech roles is supporting a median price point averaging around $765,000, which gives sellers there more breathing room than you might expect given the concession chatter elsewhere. Meanwhile, entry-level new construction in Loudoun is working much harder, leaning on concessions, rate buydowns, and incentives to get deals closed, so if you're selling in that price band, you should expect the concession conversation to come up and plan for it rather than be surprised by it.

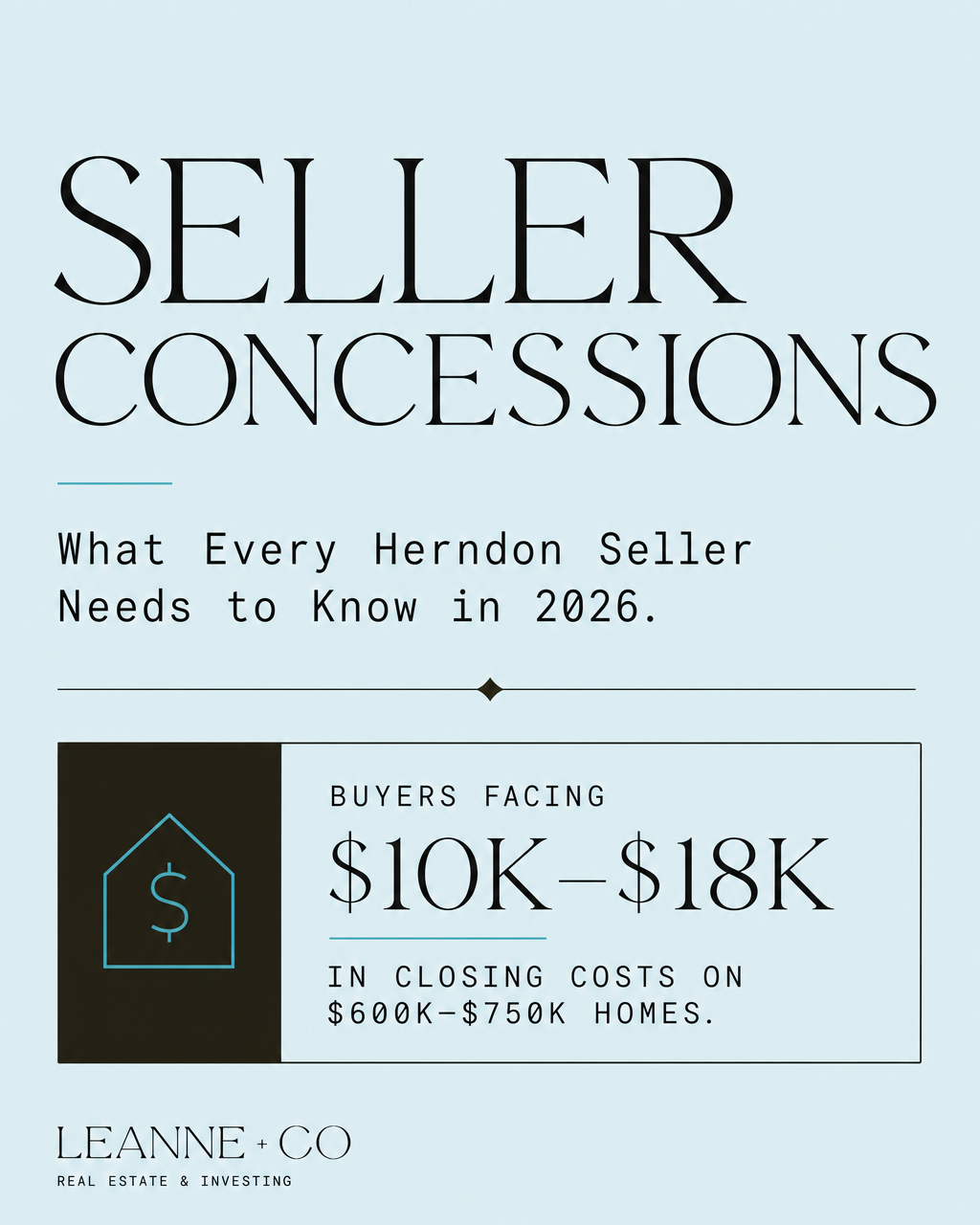

Now let's talk numbers, because this is where sellers get the most anxious. Buyers in Northern Virginia typically face $10,000 to $18,000 in closing costs on homes in the $600,000 to $750,000 range, and that gap is exactly what most concession requests aim to close. It's not arbitrary. It's a real number tied to a real settlement statement, and once you see it that way, it stops feeling like a buyer trying to take advantage of you and starts feeling like a normal part of getting to the closing table.

I'll add one thing here from my own background as a military spouse. VA loans have their own rules around what a seller can and can't contribute, and I've walked plenty of sellers through exactly how that works when their buyer is using VA financing. It's a little different from a conventional or FHA buyer, and knowing the difference up front saves everyone a headache later in the process.

The bigger truth in this market is that pricing strategy and concession strategy aren't separate conversations anymore; they're the same conversation. Once you factor in agent commissions, closing costs, seller concessions, repairs, and moving costs, your net proceeds can feel tighter than expected, but that doesn't mean your home isn't valuable. It just means this market won't automatically reward every seller the way it did a few years ago. Sellers who plan for that going in and understand which type of concession actually solves their buyer's problem tend to walk away from closing with a lot less stress than sellers who treat every request like a fight.

If you're getting ready to list in Herndon, Reston, Ashburn, or anywhere else in Fairfax or Loudoun County, this is exactly the kind of thing I sit down and map out with clients before we ever put a sign in the yard. Every submarket is different, every buyer pool is different, and the right concession strategy for a townhome in Sterling looks nothing like the right strategy for a single-family home in Vienna.

If you're thinking about making a move, buying, selling, or investing, let's talk. No pressure, just a real conversation about your options. 202-409-7513.